Restaking is one of the most significant — and most discussed — innovations in DeFi since liquid staking itself.

The core idea: once you’ve staked ETH to secure the Ethereum network, that same staked ETH can simultaneously be used to secure additional networks and services — earning additional rewards from each. Your ETH does double (or triple) duty, extending Ethereum’s security to new protocols while you earn more yield.

EigenLayer, the protocol that introduced restaking at scale, has attracted over $10 billion in restaked ETH since launching in 2023 — making it one of the fastest-growing DeFi protocols ever. But with the additional yield comes additional risk — specifically, additional slashing exposure.

This guide explains what restaking is, how EigenLayer works, what Actively Validated Services are, and what the real risks look like.

The Problem Restaking Solves

To understand restaking, you need to understand the problem new blockchain services face.

The Security Bootstrapping Problem

When a new blockchain network, oracle system, bridge, or middleware protocol launches, it needs economic security — validators who have real financial stake that can be slashed if they misbehave. Without this security, the service is cheap to attack.

Traditional approach: Build a new token, distribute it, convince validators to lock it up. Problems:

- New token has little value initially → security is weak until token price increases

- Building a validator community from scratch takes years

- Fragmented security: many different tokens securing many different services — each individually weak

EigenLayer’s approach: What if new services could “borrow” Ethereum’s existing security? ETH stakers have already committed billions to secure Ethereum. What if they could extend that security commitment — and the associated slash risk — to new services, earning additional rewards?

This is restaking: reusing staked ETH to secure additional services.

What Is Restaking?

Restaking is the process of taking already-staked ETH (or liquid staking tokens like stETH) and redeploying it to provide cryptoeconomic security to additional networks or services beyond just Ethereum itself.

Key characteristics:

- Your ETH remains staked on Ethereum (still securing the base layer)

- Simultaneously, that same ETH secures one or more additional Actively Validated Services (AVS)

- You earn staking rewards from Ethereum + rewards from each AVS you secure

- In exchange, you accept additional slashing risk from each AVS

How EigenLayer Works: The Architecture

The Participants

Stakers/Restakers: ETH holders who restake their assets. Can restake via:

- Native restaking: Running a solo validator and pointing the withdrawal credentials to EigenLayer’s smart contracts

- LST restaking: Depositing liquid staking tokens (stETH, rETH, cbETH) into EigenLayer’s contracts

Operators: Professional node operators who run the validation software for AVSs. Stakers delegate their restaked ETH to operators, who do the actual work of validating AVS tasks.

Actively Validated Services (AVSs): The protocols that pay for EigenLayer’s security. They define the rules: what operators must do, and what behavior gets slashed.

Liquid Restaking Protocols: Protocols (Ether.fi, Renzo, Puffer) that abstract the restaking process — you deposit ETH and receive a Liquid Restaking Token (LRT) while they handle the EigenLayer interaction.

The Flow

- Staker deposits: ETH staker deposits stETH (or native ETH) into EigenLayer’s contracts

- Operator selection: Staker delegates to an operator who will actively validate for AVSs

- AVS opt-in: Operator opts into one or more AVSs — accepting their slashing conditions

- Validation work: Operator runs AVS software, performs validation tasks (oracle updates, bridge attestations, DA layer confirmations, etc.)

- Reward distribution: AVS pays rewards to operators → operators distribute to stakers (after their cut)

- Slashing (if misbehavior): If operator misbehaves on an AVS, EigenLayer’s contracts slash the restaked ETH — reducing staker and operator balances

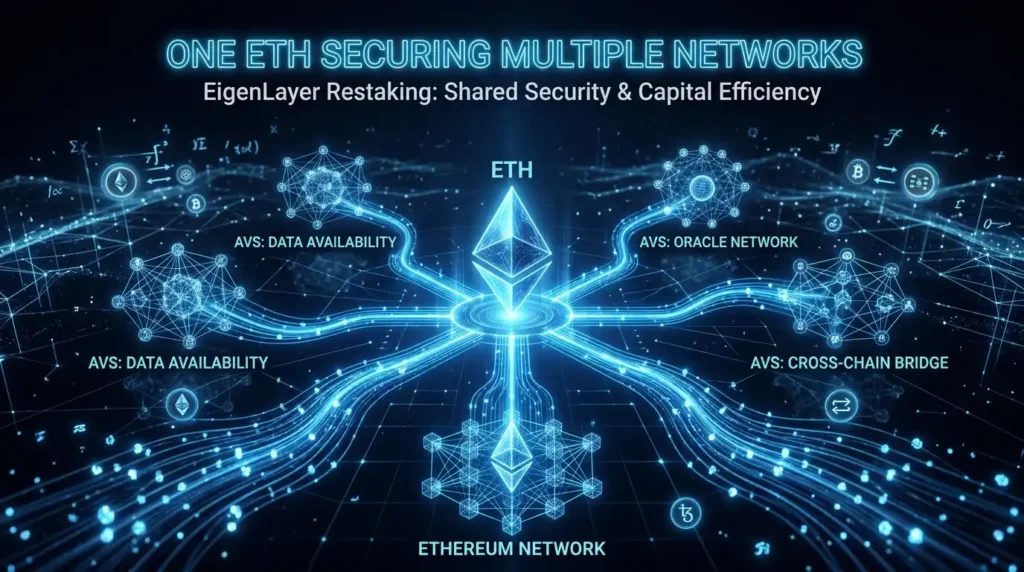

What Are Actively Validated Services (AVSs)?

AVSs are the protocols and services that use EigenLayer’s pooled security. They represent the “demand side” of the restaking marketplace.

Categories of AVSs in 2026:

Data Availability Layers:

Services that store and make available the transaction data for rollup chains. EigenDA (EigenLayer’s own AVS) competes with Celestia and other DA solutions, offering cheap, high-throughput data availability secured by restaked ETH.

Oracle Networks:

Decentralized price feeds and data delivery systems. Restaked ETH security makes oracle manipulation more expensive.

Cross-Chain Bridges:

Protocols enabling asset transfers between blockchains. Bridge security has historically been weak — bridges lose billions to hacks annually. Restaking adds cryptoeconomic security to bridge validators.

Rollup Sequencers:

Decentralized sequencers for Layer 2 networks (replacing centralized sequencers that are a single point of failure).

Keeper Networks:

Automated systems that execute on-chain actions (liquidations, order execution, smart contract automation).

Key AVSs operating in 2026:

- EigenDA: Data availability layer — the largest AVS by far

- Brevis: ZK coprocessor for smart contracts

- Lagrange: ZK state proofs

- Aligned Layer: ZK proof verification

Restaking Yields: What to Expect

Restaking adds additional reward streams on top of base ETH staking:

Base ETH staking (Lido stETH): ~3.5% APY

Restaking rewards (EigenLayer/Ether.fi): Additional 0.5–2%+ depending on:

- Number of AVSs opted into

- AVS reward rates (highly variable, many distribute their own governance tokens)

- Market demand for security from specific AVSs

Combined restaking yield (April 2026):

- Ether.fi (eETH): ~4–5% APY total (base staking + restaking)

- Renzo (ezETH): ~4–4.5% APY

- Puffer (pufETH): ~4–4.5% APY

Important context: Many restaking rewards in 2026 are still partially in points/governance tokens rather than fully in ETH or stablecoins. The long-term sustainable yield from restaking is still being established as the market matures.

Liquid Restaking Tokens (LRTs)

Just as liquid staking protocols (Lido, Rocket Pool) abstracted native ETH staking into liquid tokens (stETH, rETH), liquid restaking protocols abstract EigenLayer restaking into tradeable tokens.

How LRTs work:

- Deposit ETH to a liquid restaking protocol (Ether.fi, Renzo, Puffer)

- Protocol deposits to EigenLayer and manages operator delegation

- You receive an LRT (eETH, ezETH, pufETH) representing your restaked position

- LRT earns base staking + restaking rewards automatically

- LRT can be used in DeFi (as collateral, in LP positions)

The major liquid restaking protocols:

Ether.fi (eETH / weETH):

- Largest liquid restaking protocol by TVL (~$6B)

- Non-custodial design — validators are run by the depositor (unique among LRT protocols)

- Integrated natively with EigenLayer and multiple AVSs

- eETH can be wrapped to weETH for DeFi use (avoids rebasing complexity)

Renzo (ezETH):

- Second-largest LRT protocol

- Multi-chain (Ethereum, Arbitrum, Linea)

- REZ governance token

Puffer Finance (pufETH):

- Anti-slashing design — native validators must provide additional ETH as anti-slashing bond

- Growing TVL in 2026

Kelp DAO (rsETH):

- Multi-asset restaking (accepts stETH, ETHx, sfrxETH)

- Growing DeFi integration

EigenLayer vs Symbiotic vs Karak: The Restaking Competition

EigenLayer pioneered restaking but competitors have emerged:

EigenLayer:

- First mover, largest ($10B+ TVL)

- ETH-focused (though expanding)

- Most AVS integrations

- EIGEN token launched 2024

Symbiotic:

- Backed by Paradigm and cyber•Fund

- Multi-asset restaking (not ETH-only)

- More flexible AVS design

- Growing rapidly in 2025-2026

Karak:

- Multi-chain restaking

- Supports broader asset types

- Earlier stage

The restaking landscape remains competitive and evolving — multiple protocols may coexist serving different niches.

The Risks of Restaking

Restaking amplifies yield — and amplifies risk. Understanding these risks is essential before restaking any ETH.

1. Compounded Slashing Risk

This is the central risk of restaking. Each AVS you secure through EigenLayer has its own slashing conditions. If an operator misbehaves on an AVS — or if the AVS’s own code has a bug that triggers false slashing — your restaked ETH can be slashed.

The compounding problem:

- Native staking: 1 slashing risk (Ethereum consensus)

- Restaking across 5 AVSs: potentially 6 slashing risks (Ethereum + 5 AVSs)

A slashing event that might cause 5% loss from one AVS becomes significant when you’ve opted into multiple. And unlike Ethereum’s well-tested consensus rules, AVS slashing conditions may be newer and less battle-tested.

In practice: Major slashing events have been rare in EigenLayer’s early operation (2023-2026). But the theoretical risk is real and increases with the number of AVSs secured.

2. Smart Contract Risk (Multiple Layers)

Restaking adds additional smart contract layers:

- EigenLayer’s contracts (managing restaking and slashing)

- Each AVS’s contracts

- Liquid restaking protocol contracts (if using Ether.fi, Renzo, etc.)

More contracts = more attack surfaces. Each layer has been audited, but no contract is hack-proof.

3. Operator Risk

Your restaked ETH’s safety depends partly on the operator you delegate to. Operators who:

- Opt into too many AVSs without proper infrastructure

- Run buggy software for an AVS

- Have poor uptime affecting AVS performance

…can expose you to slashing even if you haven’t done anything wrong yourself.

Mitigation: Choose operators with strong track records, appropriate AVS selection, and transparent operations.

4. Liquidity Risk for LRTs

LRTs (eETH, ezETH) are derivatives — they can trade at a discount to ETH during market stress (similar to stETH’s historical depeg risk, but potentially more severe given the additional complexity).

If you’re using an LRT as DeFi collateral and it depegs significantly, you could face liquidation.

5. AVS Failure/Abandonment Risk

AVSs are new protocols — some may fail to attract meaningful usage, reduce or eliminate rewards, or shut down. If AVS rewards dry up, restaking yield declines — but you still carry the slashing risk from having opted in.

6. Regulatory Risk

Restaking is a relatively new concept and regulatory treatment is unclear. The EU’s MiCA framework doesn’t specifically address restaking, and US regulators haven’t issued clear guidance.

Restaking vs. Staking: A Comparison

| Native Staking | Liquid Staking | Restaking | |

|---|---|---|---|

| Yield | ~3.5% APY | ~3.4–3.8% APY | ~4–5%+ APY |

| Slashing risk | Ethereum only | Ethereum (via Lido/RP) | Ethereum + AVSs |

| Complexity | High (solo) / Low (LST) | Low | Medium-High |

| Liquidity | Low (locked) | Full (LST tradeable) | Full (LRT tradeable) |

| Smart contract risk | Low | Medium | High |

| Best for | Long-term ETH believers, decentralization | Most ETH holders | Yield-seeking, DeFi-native users |

How to Restake: The Options

Option 1: Native Restaking (Advanced)

- Run an Ethereum validator with 32 ETH

- Set withdrawal credentials to EigenLayer’s pod contract

- Delegate to an operator via EigenLayer’s interface

- Opt into specific AVSs (or let operator handle this)

Best for: Large ETH holders comfortable running infrastructure.

Option 2: LST Restaking via EigenLayer (Intermediate)

- Acquire stETH (from Lido) or rETH (from Rocket Pool)

- Go to app.eigenlayer.xyz

- Deposit stETH into EigenLayer

- Delegate to an operator

- Your stETH is now restaked — earning base staking + operator-distributed AVS rewards

Note: Direct EigenLayer deposits typically have withdrawal delays. Check current withdrawal conditions.

Option 3: Liquid Restaking Protocol (Easiest)

- Go to app.ether.fi, app.renzoprotocol.com, or app.puffer.fi

- Deposit ETH → receive eETH/ezETH/pufETH

- LRT automatically earns staking + restaking rewards

- Use LRT in DeFi if desired

Best for: Most DeFi users — simple, liquid, no operator management.

Key Terminology

Restaking: Reusing staked ETH to simultaneously secure additional networks/services beyond Ethereum, earning additional rewards.

EigenLayer: The primary restaking protocol on Ethereum — the marketplace connecting restakers, operators, and AVSs.

AVS (Actively Validated Service): A protocol or service that uses EigenLayer’s pooled security to secure its operations.

Operator: A professional node operator who runs AVS software and validates on behalf of restakers.

LRT (Liquid Restaking Token): A derivative token received from liquid restaking protocols (eETH, ezETH, pufETH) — tradeable and usable in DeFi.

Slashing (restaking): Confiscation of restaked ETH for operator misbehavior on an AVS — additional risk layer vs. native staking.

EigenDA: EigenLayer’s own data availability AVS — largest by usage.

EIGEN token: EigenLayer’s governance/intersubjective staking token — used for AVS tasks that can’t be objectively slashed.

The Bottom Line

Restaking represents a genuine innovation: a marketplace for Ethereum’s cryptoeconomic security that allows new services to bootstrap security without building from scratch.

For users, the honest assessment:

- Additional yield of 0.5–2% above liquid staking — real but modest

- Additional slashing risk — real and growing as more AVSs launch

- Additional smart contract complexity — meaningful risk for a new paradigm

Who should consider restaking:

- ETH holders comfortable with DeFi mechanics who want to maximize yield on long-term ETH holdings

- Users who understand and accept the additional risk layers

Who should not restake (yet):

- Beginners who haven’t mastered basic liquid staking first

- Users who can’t monitor complex positions

- Anyone who can’t afford to lose the additional portion of ETH that might be slashed

The simplest path: If you want restaking exposure, use Ether.fi (eETH) on Arbitrum or Base — deposit ETH, receive eETH, earn combined staking + restaking yield automatically. Start small. 🔄

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. Restaking involves significant risks including slashing, smart contract vulnerabilities, and total loss of restaked capital. Always conduct your own research.

")

in DeFi? Complete Guide (2026)")

{kind=link}